PQ in the equation of exchange represents the total value of all purchases made with a cryptocurrency.

There are two ways to find total purchases.

The first is through direct, on-chain observation. The second is to use orthogonal metrics as a proxy for on-chain data.

Estimating PQ

Estimating PQ through proxy metrics is useful where data is unclear.

For example, Monero, whose chain can’t be surveilled – is impossible to gather data from.

XMR transaction amounts are hidden, and transaction histories are unclear.

XMR is mainly used on the dark web – exactly like Bitcoin when it started.

If you know the volume of purchases on the dark web, and the percentage of dark web transactions using Monero, you have a large component of PQ for XMR.

Finding PQ On-chain

In transparent blockchains, data is easy to parse.

Most blockchains are transparent, so on-chain data can be used as inputs to the equation of exchange.

It’s easiest to do this for Ethereum-based tokens. Transaction data can be interpreted according to documentation for the smart contract, which makes it easy to identify which transactions are speculative and which are to be included as part of total purchases.

For example, you can look at a Chainlink (LINK) transaction and understand which tokens are being paid to data providers, and which are simply being sent between exchanges by arbitrage traders.

[LINK dashboard Dune Analytics]

Etherscan is a helpful site to find known addresses like exchange wallets. Dune Analytics is a visualization platform with crowdsourced insights.

Combining Methods

Transparent medium-of-exchange coins, especially those which are UTXO-based (Dash, Litecoin, Bitcoin Cash) require a combination of on and off-chain analysis to find PQ for the equation of exchange.

It’s not always clear which transactions are self-sends, speculative purchases, or those sent to mixers for obfuscation, etc.

In this case, it’s helpful to identify known wallets and work from there.

Exchange addresses are publicly available, flagged on sites like Etherscan and Dune Analytics.

We use these frameworks to design valuable tokens.

If you’re interested in building a token with fundamental value or valuing cryptocurrencies with a simple framework, reach out to us for a free consult.

Market cap, short for market capitalization is a misleading metric when valuing cryptocurrencies.

Market cap is borrowed from traditional finance’s equity valuation methods. Cryptocurrencies and tokens are valued using the equation of exchange.

Types of supply

The cryptocurrency space has started to recognize the inadequacy of “market cap” in valuing cryptocurrencies.

Popular metrics now distinguish between issued supply, and total supply at some later date – fully diluted market cap.

This is only a partial solution, since not even all coins which have been issued are still in circulation (e.g. Satoshi’s coins).

Circulating supply in the Eat Sleep Crypto valuation framework refers to only those coins which have moved in a time frame.

The time frame is arbitrary; it’s only important that the other components of the equation of exchange use the same one.

Why circulating supply is best

The most meaningful comparisons can only be made by looking at different sets of coins – i.e. coins with the same Cryptocurrency Valuation Methods; Determining Coin Age at different dates.

Looking at circulating supply allows more useful comparisons of velocity and supply for the same coin over time.

The equation of exchange is as old as economics itself.

First derived by John Stuart Mill, then referenced by Adam Smith, the equation of exchange has gained popularity more recently through Milton Friedman and other monetary theorists.

The equation of exchange, MV = PQ is an algebraic equation used to solve for various components of a currency’s value.

It is typically used by economists to find the necessary supply of a currency – or, the minimum value of the monetary baseneeded for commerce.

When not enough fiat currency circulates, notes trade above their face value.

Cryptocurrencies experience the same demand pressure, but since cryptocurrency prices are floating, their prices appreciate to meet demand for purchases.

Increasing demand pressure and decreasing circulating supply causes a cryptocurrency’s price floor to increase.

If a cryptocurrency’s price on exchanges is close to its price floor – the price below which it cannot sustainably trade – the traded price must also increase to meet demand for value to be transferred through it.

All else equal, a cryptocurrency or token with a larger Total Addressable Market, following the principles of tokenomics, will have a higher price.

Components of Total Addressable Market

A currency’s TAM and its components come from each of its use cases.For example, Ethereum’s native token, ETH has multiple Total Addressable Markets.

ETH is used to pay fees for all of the applications running on the Ethereum network. Demand for payment of ETH fees is one component of its Total Addressable Market.

ETH also used to collateralize other tokens – Dai, for example. So another of ETH’s Total Addressable Market is use as collateral.

This in turn comes from demand for Dai (a stablecoin with many uses) and varies with Dai’s capture of its Total Addressable Market.

To maximize ETH’s fundamental value or price floor, these two use cases must be maximized.

When seeking to maximize a token’s price, TAM should be made large.

This is generally done by having a token transfer large amounts of value, or giving it many uses.

Fundamentally, cryptocurrencies get their value through use as a medium of exchange. This includes cryptocurrencies paid for goods and services, and tokens paid for fees, collateral, and other tokenomic levers within a protocol.

Most cryptocurrencies and tokens are best valued using the equation of exchange.

The equation of exchange was first derived by John Stuart Mill, referenced by Adam Smith, and popularized by Milton Friedman.

For example, if CashCoin is used to buy $1,000,000 worth of products per year, and each CSH is used an average of 5 times, the variables are as follows:

Coins which are lost, locked up, or in cold storage are not part of an economy – they’re not subject to supply and demand.

Stored coins may be relevant to speculators, but speculation is not priced in directly; the price floor of a cryptocurrency and its speculative price premium are different.

Price floor vs speculative price premium

A cryptocurrency’s price reflects:

Fundamental value, price floor

Speculative price premium

Cryptocurrency price floors

Fundamental value reflects supply and demand for a cryptocurrency as a medium of exchange.

This fundamental value is a price floor – a price a currency will not sustainably trade below.

When a currency trades at its price floor, volatility will naturally cause it to dip below, but buying pressure from aggregate demand brings the price back up.

A currency might trade below its price floor, but not for long.

Speculative price premium

The rest of a cryptocurrency’s price is speculative.

It may be rational to price in future returns (see Burniske’s DEUV), but it makes sense to distinguish speculative premium from fundamental value.

Price/price floor ratio is a meaningful measure of risk/reward – the closest

Most cryptocurrencies’ price floor can be extrapolated from on-chain data.

Identifying price floors using on-chain data

Dune Analytics is a free, open-source chain analytics platform.

Price floors can be worked out using on-chain analytics.

The components of price floors – circulating supply, velocity, and total purchases are all found on-chain.

Some on-chain data, like ERC-20 token data is easy to interpret. ERC-20 transactions are easy to reconstruct from blockchain analysis.

Commercial transactions on medium-of-exchange currencies are harder to distinguish from speculative trading, self-transfers, mixing, but it can be done.

Determining which transactions are speculative, self-transfers, part of mixers using just metadata requires getting creative.

Conclusion

This cryptocurrency valuation framework is used to identify and take advantage of price floors, calculate risk/reward ratios, and engineer tokens with price floors using the principles of tokenomics.

If you’ve spent any time on this site, you’re likely familiar with the Equation of Exchange, MV = PQ.

This simple equation, first derived by John Stuart Mill and later popularized by Milton Friedman is the foundation of all our work.

The equation of exchange can be applied at a high level to quickly calculate price floors of a currency based on a few inputs or assumptions.

It can also be applied at a micro-level to tweak the economics and incentives of a cryptocurrency or token for maximum value capture.

If any of these terms are unfamiliar, you can refer to the Glossary page for their definitions.

Goals of this project

Token analysis script

Token flow visualization

Token engineering framework

Token economic analysis

The first goal of this project is to create a script that parses transaction data of a given cryptocurrency or token in order to find components of its price floor according to the equation of exchange, MV = PQ.

Simple pulls include contract events and token transactions that take place within the token protocol to find PQ. Calculated components include circulating supply and address balances over time to find V.

Token flow model

Using variants of the equation of exchange, token flow can be modeled within an ecosystem.

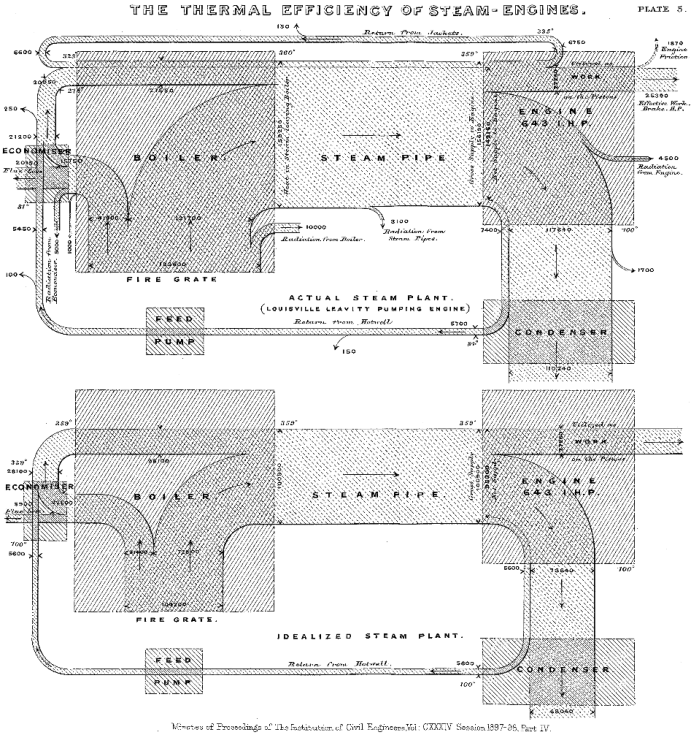

A novel way to do this is by using a Sankey diagram.

The Sankey diagram takes its name from Irish Captain Matthew Sankey, who used it to model the energy efficiency of a steam engine.

Sankey compared the real energy efficiency of an engine to its ideal efficiency.

While Sankey was interested in energy efficiency, we are interested in value capture.

Value is most commonly captured by tokens when they are used as a medium of exchange, denominated in another separate unit of account – e.g. an expenditure of $10,000 worth of Bitcoin.

Components in a token flow diagram

Objects in a token flow diagram represent participants in the ecosystem within which a token circulates.

Value transferred via transactions is represented by the connections in between.

The dimensions (height x width x length = volume) of the “pipes” representing these connections represent:

Tokens circulating in an ecosystem (circulating supply)

The value transferred between participants in an ecosystem (PQ)

The time a token takes to circulate, represented by length of all pipes (V)

Token flow diagrams denominated in native units (e.g. BTC) and those denominated in another unit of account (dollars) can be overlayed to solve for the price floor of each unit.

In this way, token flow diagrams become a visual aid in calculating price floors.

Token economic engineering

Sankey diagrams are fitting for token flow visualization for more than one reason.

Sankey’s hallmark example of a steam engine makes for an excellent analogy to token ecosystems for our purposes of designing and refining the token economics of a protocol, token economic engineering.

Like steam engines, cryptocurrency protocols have mechanisms which direct the flow and efficiency of energy.

In our models, energy is economic “potential” energy, represented by tokens with purchasing power.

Keeping with the steam engine analogy, the “goal” of token economic engineering is to first to increase the volume of the pipes, and second to decrease the number of tokens flowing through them.

We discuss various ways to do this on Telegram, and we collaborate with each other in reaching the goals described above.

If you’d like to collaborate, send a message to @EatSleepCrypto on Twitter for an invite.

Bitcoin has been on some wild rides the past few years. Hitting a crescendo of $20,000 in December 2017, BTC dropped to $12,000 just days later and stumbled down to $6,200 over the next two months.

Many people panicked: some trading in and out, others HODLing all the way down. Weathering 80% losses takes discipline, but the promise that Bitcoin might boom again keeps speculators invested. Bitcoin’s history of consistent, outrageous returns is compelling for those taking a long view. “Taking a long view” requires understanding three principles: objective valuation, technical developments, and factors surrounding adoption.

For traditional investors, this speculation looks foolish. “Where are the fundamentals?” they ask. Volatile returns engender speculation, and speculation spawns volatility. High volatility plus a lack of a traditional valuation mechanism generally screams ‘pyramid scheme’ and forces more conservative investors to abandon the field to speculators. And round and round we go.

Cryptocurrency Valuation

Bitcoin, like all currencies, derives its value through use as a medium of exchange, and I’ve already demonstrated that it can be valued according to the accepted equation of exchange: MV = PQ. This equation shows that the price of a currency must be high enough to support the purchases made with it.

To illustrate this principle, let’s imagine Alice wants to buy a car from her friend Bob. (yes, for the love of Mike, it’s Alice and Bob again). Both Bob and Alice agree that the car is worth $1,000, but Bob demands to be paid in his own currency: Bob’s Car Coins (BCC).

The question immediately arises, how much is each BCC worth?

For an established currency, we could look to market data, but there is none. BCC is an entirely new currency.

Let’s say Bob wants 10 BCC for his car, but Alice has no BCC. Assuming she can exchange dollars for BCC, Alice is willing to pay up to $100 per BCC in order to purchase the car (10 BCC multiplied by $100 per BCC equals $1,000.)

In this transaction, Bob doesn’t explicitly tell Alice the price of each BCC, but he does give his currency value by choosing to accept payments in it. In this example, we see the axiom that the value of a currency increases to support the purchases being made with it.

Speculation can move prices temporarily, but use as payment establishes a currency’s worth.

There are two aspects to the determination of value through fundamental analysis: applying economic principles, and data extrapolation. In cryptocurrency valuation, the second informs the first.

Economic Principles

As illustrated in the example, using a currency as a medium of exchange gives it value. We see this principle applied in the equation of exchange. Fundamentally, if we know the total value of purchases with a cryptocurrency and the velocity of the currency, we can determine the price of each unit. Velocity is the average number of times a unit is ‘recycled’ in a specified time frame. With these variables, the equation of exchange (MV = PQ) is easy to solve algebraically.

Rewritten to solve for M, the monetary base, the equation of exchange reads M = PQ/V. You can read the full explanation in previous Eat Sleep Crypto articles. In short, this means that the value of circulating currency is equal to the total value of purchases made with that currency, divided by the average number of times a unit of currency changes hands.

After solving for M, we can determine the value of each unit by dividing M by the circulating supply of each coin. We do this in several examples on Eat Sleep Crypto, including the Investor Series #1 – Bitcoin valuation article.

Data Extrapolation

While it appears satisfying and conclusive, fundamental analysis is not the only approach to currency valuation. We can also forecast future prices based on expected use of cryptocurrencies as a medium of exchange. In the Bitcoin article, we use the SWIFT network as a proxy for global transactions. Data extrapolation, in this case, involves substituting Bitcoin for the SWIFT network. Our model yields a conservative estimate of $50 million per bitcoin by 2030, employing our own assumptions. (If you’re interested in seeing a copy of our model, say something in the comments below.)

$50 million per bitcoin may sound like hyperbole. It’s not. The SWIFT network does over a quadrillion dollars in transactions per year: a thousand trillions!

This analysis doesn’t factor in transactions from commercial payment systems like Visa and Mastercard, Paypal, or cash payments, all of which are vulnerable to replacement by crypto. But, it does assume adoption of crypto as a medium of exchange, when in reality immediate adoption is not the top priority for most cryptocurrency developers.

Despite the justifications referenced above, some proponents of Bitcoin continue to dismiss it as a medium of exchange. There are two reasons why. The first is the “store of value” narrative and the second is Bitcoin’s “greater fool” theory.

Bitcoin: A Peer-To-Peer Electronic Store Of Value

People who promote Bitcoin as a “store of value” argue against its use as a medium of exchange. Discounting entirely that Bitcoin is far too volatile to be a store of value in the short term, there is so much irony in this position. As good “stores of value” need fundamental properties to make them desirable, good currencies are inherently stores of value and command higher prices because of it.

The long term value proposition of Bitcoin or any other cryptocurrency is significantly greater as a medium of exchange than as a store of value. Estimates of Bitcoin’s value if it replaced gold entirely is only $4 million dollars per coin. That’s more than an order of magnitude less than its conservative value as a medium of exchange.

While the BTC community fritters away it’s first-mover advantage, most other cryptofolk are driving adoption where it’s needed least. If you think of cryptocurrencies as products solving a problem, you can’t help but see that the largest markets, in terms of numbers of customers, are being ignored

A large percentage of early Bitcoiners have first-world origins. Adoption evangelists have therefore been active in those countries – exactly where a volatile, traceable, alternative currency is of little use. While BTC supporters have rejected Bitcoin’s purpose as a peer-to-peer electronic cash system, even those who imagine scaling via the Lightning Network haven’t considered the technical and economic limitations of third-world users. Not to mention the limitations of the Lightning Network itself!

Bitcoin’s Greater Fool Theory

Some advocates of Bitcoin believe that others will purchase Bitcoin because of greed and fear of missing out. As a consequence, they drive the price up. These advocates assume BTC can scale and that it will eventually become a store of value once it reaches its final price. In their minds, this culminates with institutions FOMOing into BTC as an investment.

These arguments imply that cryptocurrencies have no fundamental drivers of value. In reality, cryptocurrencies have a stronger value proposition than almost any other asset class. Because of blockchain’s transparency, we’re able to quantify cryptocurrencies’ worth.

The Importance of Adoption

Many cryptocurrency advocates across communities imagine that cryptocurrency will take hold in places like the US and Europe, and then gradually catch on in third world countries.

The reality is, first world users don’t need Bitcoin. But Venezuelans do.

Ironically, if adopted as a medium of exchange or “means of payment”, cryptocurrencies would see less volatility and eventually be adopted by the first world for payments. This decrease in volatility happens within an economy as purchases of the currency happen more frequently. A larger volume of commercial transactions offsets currency volatility. Further stability comes as goods and services are denominated in it.

Price Denomination

The denomination of goods and services in a currency creates strong price support. A quick thought experiment suggests that if someone knows they can buy the same meal for 0.1 BCH each time, they’re able to benchmark the price of other things in it, too. The axiom here is that people value a currency based on what it buys.

This is the same principle we see in our illustration with Alice and Bob. We can value each BCC Alice received from Bob at $100, despite neither of them officially setting the price. In this case, it was because we know that each BCC got Alice 1/10th of a $1000 car.

Closing Thoughts

With widespread adoption as a medium of exchange, Bitcoin, or any cryptocurrency, will become more stable due to the volume of purchases.

The key here is that ‘stability’ is relative. It’s relative to the price of goods, and the price of other currencies. Compared to a currency like Venezuela’s bolivar with 1,000,000% inflation against the USD, Bitcoin’s 80% drop is nothing. Fittingly, it’s through adoption in countries like Venezuela that cryptocurrencies can gain the necessary stability for worldwide adoption, while filling desperate demand for a sound currency.

With all this in mind, I was thrilled to hear about Bitcoin.com’s recent announcement of the initiative to onboard 500 merchants a month in Venezuela. Adoption like this raises prices and reduces volatility. The more adoption a cryptocurrency has as a medium of exchange, the more valuable it will be, and unlike a purely speculative asset, its volatility actually decreases with volume.

I’m looking forward to seeing meaningful adoption of all cryptocurrencies, and eager to see the shift in focus of cryptocurrency users from speculation to fundamentals as we witness the benefits that cryptocurrencies bring to the world.

Yesterday, JP Morgan Chase & Co released a note on Bitcoin’s intrinsic value.

Their analysis suggests Bitcoin is overvalued at $8000, citing a deviation from the costs of production.

BTC is overvalued, but not because miners are making a profit.

This argument has been floating around the Bitcoin space for a while. The position JPM takes is that “price follows hash.”

It’s also called the Labor Theory of Value and has been popularized by fans of Karl Marx.

The Labor Theory of Value opposes common sense; products are not valuable because they take effort but because they have demand, which implies utility.

Why Price Appears To Follow Hash

Price and hash are strongly correlated, but few take the leap of suggesting an increase in hashrate causes price to increase.

In March, Eat Sleep Crypto newsletter subscribers learned the mechanism behind the seeming causation.

Many Bitcoiners recognize a relationship between price and mining power (hash). The debate has been reduced to “price follows hash” vs “hash follows price.”

As usual, the truth is nuanced.

In a bull market, hash follows price. Miners choose to mine the most profitable coin.

In a bear market, price follows hash as miners with different costs undercut each other.

BTC dropped from $6200 to $3200 during the BCH/BSV hash war in November. The drop from $6200 to $5600 saw 30% drop in hash rate from the network. At the time, 70% of Bitcoin miners were in China.

It was logical to conclude the 30% became unprofitable and switched off, leaving the rest to sell at whatever price buyers would negotiate. I’d read that the cost of mining in China was around $3200 and placed my bets accordingly.

BTC bounced at $3150.

This was a confirmation of my theory and spurred further thoughts on how to fundamentally value cryptocurrencies.

During this time, we also saw refutations of competing theories – namely that “price follows hash,” or Marx’s Labor Theory of Value. Both Bitcoin Cash (BCH) and Bitcoin (SV) saw a surge in hash power, yet both of their prices decreased over the hash war.

Excerpted from the ESC newsletter, 3/27/19

In a bull market, hash follows price. In a bear market, price only appears to follow hash.

This framework explains the seeming correlation of price and hashrate in a bear market. Hopefully, it puts Bitcoin-related discussion of the Labor Theory of Value to rest.

If you enjoyed this article, check out the rest of the articles in the cryptocurrency valuation category.