The equation of exchange, MV = PQ is foundational to the Eat Sleep Crypto valuation framework. The following articles explain each component in detail:

Imagine an auto mechanic needs to purchase $10,000 worth of parts from China. The seller demands payment in CNY, which is traded on exchanges.

To complete the payment, there must be at least $10,000 worth of Chinese Yuan in circulation.

If there isn’t at least $10,000 worth of CNY in circulation, there are two ways to make it so:

1) CNY is printed by some means, and acquired by the buyer to complete his purchase.

Or,

2) The entire circulating supply is bought up on order books until the buyer’s CNY is worth $10,000.

The first method acts on the supply side, increasing the circulating supply.

The second is based on demand, where the currency’s price appreciates to meet demand for its use.

Valuing Cryptocurrencies With the Equation of Exchange

Our microeconomic example of the equation of exchange using CNY works the same at scale, with a couple more moving parts.

Since cryptocurrencies can’t be inflated at will, the buying up of cryptocurrencies and tokens on exchanges for actual use cases is how price discover occurs.

Let’s say Bitcoin is used to buy $100 billion worth of goods and services annually. We’ll imagine that 10 million BTC are in the circulating supply – they not lost or otherwise unavailable. And we’ll say that each bitcoin moves between 5 people per year, on average (historical velocity of the dollar).

So our velocity is 5.

So we have M = $100 billion (PQ)/ 5 (V) = $20 billion

Applied to cryptocurrencies, this fundamental value is a *price floor* – the minimum sustainable price of a cryptocurrency, absent speculation. Dividing $20 billion by 10 million BTC to get the price per unit gives us a price floor of $10,000 per Bitcoin.

In the Investor Series articles, we find price floors of various cryptocurrencies using models with adjustable assumptions.

Circulating supply is the number of coins (cryptocurrencies, tokens) in circulation.

It can be defined different ways – the key is that it’s defined the same across components of the equation of exchange.

For example, if circulating supply means “coins which moved within the past year,” the velocity, monetary base, and total purchases should also reference those specific coins.

Generally, it’s helpful to define circulating supply to include coins with a coin age less than one year, and exclude coins on-exchange, staked, and burned.

The equation of exchange is as old as economics itself.

First derived by John Stuart Mill, then referenced by Adam Smith, the equation of exchange has gained popularity more recently through Milton Friedman and other monetary theorists.

The equation of exchange, MV = PQ is an algebraic equation used to solve for various components of a currency’s value.

It is typically used by economists to find the necessary supply of a currency – or, the minimum value of the monetary baseneeded for commerce.

When not enough fiat currency circulates, notes trade above their face value.

Cryptocurrencies experience the same demand pressure, but since cryptocurrency prices are floating, their prices appreciate to meet demand for purchases.

Increasing demand pressure and decreasing circulating supply causes a cryptocurrency’s price floor to increase.

If a cryptocurrency’s price on exchanges is close to its price floor – the price below which it cannot sustainably trade – the traded price must also increase to meet demand for value to be transferred through it.

Fundamentally, cryptocurrencies get their value through use as a medium of exchange. This includes cryptocurrencies paid for goods and services, and tokens paid for fees, collateral, and other tokenomic levers within a protocol.

Most cryptocurrencies and tokens are best valued using the equation of exchange.

The equation of exchange was first derived by John Stuart Mill, referenced by Adam Smith, and popularized by Milton Friedman.

For example, if CashCoin is used to buy $1,000,000 worth of products per year, and each CSH is used an average of 5 times, the variables are as follows:

Coins which are lost, locked up, or in cold storage are not part of an economy – they’re not subject to supply and demand.

Stored coins may be relevant to speculators, but speculation is not priced in directly; the price floor of a cryptocurrency and its speculative price premium are different.

Price floor vs speculative price premium

A cryptocurrency’s price reflects:

Fundamental value, price floor

Speculative price premium

Cryptocurrency price floors

Fundamental value reflects supply and demand for a cryptocurrency as a medium of exchange.

This fundamental value is a price floor – a price a currency will not sustainably trade below.

When a currency trades at its price floor, volatility will naturally cause it to dip below, but buying pressure from aggregate demand brings the price back up.

A currency might trade below its price floor, but not for long.

Speculative price premium

The rest of a cryptocurrency’s price is speculative.

It may be rational to price in future returns (see Burniske’s DEUV), but it makes sense to distinguish speculative premium from fundamental value.

Price/price floor ratio is a meaningful measure of risk/reward – the closest

Most cryptocurrencies’ price floor can be extrapolated from on-chain data.

Identifying price floors using on-chain data

Dune Analytics is a free, open-source chain analytics platform.

Price floors can be worked out using on-chain analytics.

The components of price floors – circulating supply, velocity, and total purchases are all found on-chain.

Some on-chain data, like ERC-20 token data is easy to interpret. ERC-20 transactions are easy to reconstruct from blockchain analysis.

Commercial transactions on medium-of-exchange currencies are harder to distinguish from speculative trading, self-transfers, mixing, but it can be done.

Determining which transactions are speculative, self-transfers, part of mixers using just metadata requires getting creative.

Conclusion

This cryptocurrency valuation framework is used to identify and take advantage of price floors, calculate risk/reward ratios, and engineer tokens with price floors using the principles of tokenomics.

If you’ve spent any time on this site, you’re likely familiar with the Equation of Exchange, MV = PQ.

This simple equation, first derived by John Stuart Mill and later popularized by Milton Friedman is the foundation of all our work.

The equation of exchange can be applied at a high level to quickly calculate price floors of a currency based on a few inputs or assumptions.

It can also be applied at a micro-level to tweak the economics and incentives of a cryptocurrency or token for maximum value capture.

If any of these terms are unfamiliar, you can refer to the Glossary page for their definitions.

Goals of this project

Token analysis script

Token flow visualization

Token engineering framework

Token economic analysis

The first goal of this project is to create a script that parses transaction data of a given cryptocurrency or token in order to find components of its price floor according to the equation of exchange, MV = PQ.

Simple pulls include contract events and token transactions that take place within the token protocol to find PQ. Calculated components include circulating supply and address balances over time to find V.

Token flow model

Using variants of the equation of exchange, token flow can be modeled within an ecosystem.

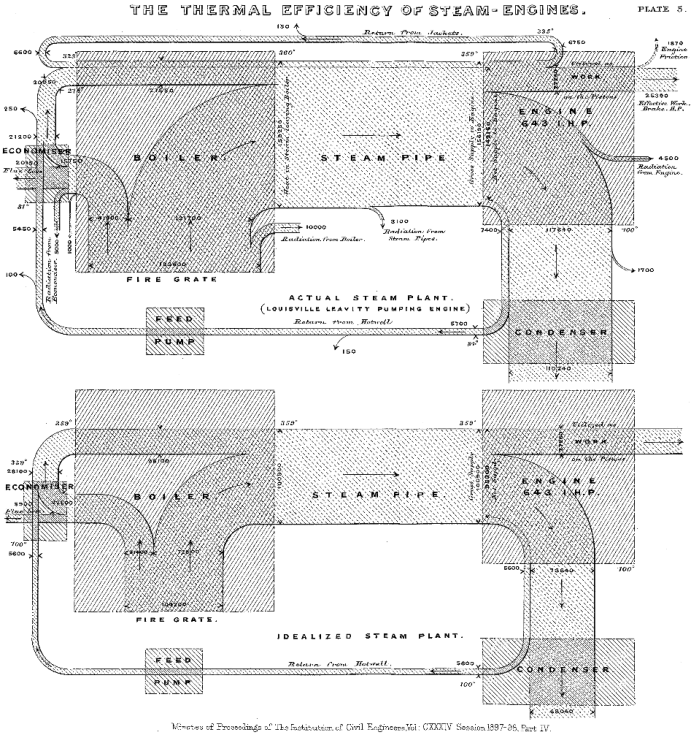

A novel way to do this is by using a Sankey diagram.

The Sankey diagram takes its name from Irish Captain Matthew Sankey, who used it to model the energy efficiency of a steam engine.

Sankey compared the real energy efficiency of an engine to its ideal efficiency.

While Sankey was interested in energy efficiency, we are interested in value capture.

Value is most commonly captured by tokens when they are used as a medium of exchange, denominated in another separate unit of account – e.g. an expenditure of $10,000 worth of Bitcoin.

Components in a token flow diagram

Objects in a token flow diagram represent participants in the ecosystem within which a token circulates.

Value transferred via transactions is represented by the connections in between.

The dimensions (height x width x length = volume) of the “pipes” representing these connections represent:

Tokens circulating in an ecosystem (circulating supply)

The value transferred between participants in an ecosystem (PQ)

The time a token takes to circulate, represented by length of all pipes (V)

Token flow diagrams denominated in native units (e.g. BTC) and those denominated in another unit of account (dollars) can be overlayed to solve for the price floor of each unit.

In this way, token flow diagrams become a visual aid in calculating price floors.

Token economic engineering

Sankey diagrams are fitting for token flow visualization for more than one reason.

Sankey’s hallmark example of a steam engine makes for an excellent analogy to token ecosystems for our purposes of designing and refining the token economics of a protocol, token economic engineering.

Like steam engines, cryptocurrency protocols have mechanisms which direct the flow and efficiency of energy.

In our models, energy is economic “potential” energy, represented by tokens with purchasing power.

Keeping with the steam engine analogy, the “goal” of token economic engineering is to first to increase the volume of the pipes, and second to decrease the number of tokens flowing through them.

We discuss various ways to do this on Telegram, and we collaborate with each other in reaching the goals described above.

If you’d like to collaborate, send a message to @EatSleepCrypto on Twitter for an invite.

This article is based on a Twitter conversation with Adrian X and Tao Jones, two of my favorite Bitcoiners.

I am consistently impressed with their creativity, open-mindedness, and articulation of arguments; they are worth following.

Transaction Volume and Decentralization

Each of Bitcoin’s three major forks can be summarized by their ideological preference for these two characteristics: transaction volume, and decentralization.

All of Bitcoin’s forks agree that censorship resistance is desirable. However, Bitcoin, Bitcoin Cash, and Bitcoin Satoshi Vision have different ideas of how to achieve it.

Bitcoin started as a way to make payments which couldn’t be censored. We call this quality ‘censorship resistance.’

Censorship resistance is achieved through Bitcoin’s incentives, which encourage a level of decentralization.

Bitcoin (BTC)

The fork of Bitcoin which kept the BTC ticker is mostly focused on decentralization.

BTC achieves decentralization at the base layer, but the community has become so fixated on decentralization, it’s forgotten the original goal.

Rather than peer-to-peer electronic cash, BTC is becoming a settlement layer – too expensive to use in daily transactions.

While the main chain is still ‘decentralized,’ using BTC for payments will soon require the trusted third parties Satoshi sought to eliminate.

The BTC community’s fetishizing of decentralization keeps forcing it further and further from its original purpose as a permissionless medium of exchange.

Bitcoin Satoshi Vision (BSV)

Bitcoin’s latest incarnation, Bitcoin SV aims for censorship resistance of everything.

BSV doesn’t limit censorship resistance to just transactions. It wants to include all types of data – photos, videos, documents – the whole internet on BSV.

This is entirely possible, but at the cost of significant levels of decentralization.

Bitcoin SV advocates frequently and aggressively assert that BSV can scale.

Of course it can – as can Facebook Coin, JP Morgan, and Hashgraph.

They all sacrifice decentralization.

Decentralization

Decentralization is necessary to offset systemic risk.

Unfortunately, in the hostile environment of the modern world, incentives within the protocol are not enough deter bad actors from outside it. Because all BSV miners will be known at scale, they could be forced to censor transactions.

Bitcoin Cash (BCH)

BSV sacrifices decentralization for censorship resistance of increased transaction volume.

BTC sacrifices its utility altogether.

BCH strives for sufficient levels of each in order to maximize its utility as a medium of exchange.

Decentralization exists on a spectrum; transaction throughput is high enough when all demand for payments is filled.

BCH is not perfect – it suffers from the same governance problems as the other forks.

But it’s the only fork of Bitcoin which has its priorities straight.

For different reasons, BTC and BSV miss the forest for the trees.

BCH is solving for Bitcoin’s intended use, as a medium of exchange.

Valuing Cryptocurrencies

BTC and BSV advocates also rationalize that their use cases will give their coin value.

These are topics for another post, but utility as a data store doesn’t make BSV very valuable, and Metcalfe’s Law is mostly relevant to BTC because it’s a pyramid scheme.

This is not a unilateral endorsement of BCH; each of these three currencies could succeed in their own way.

However, BTC and BSV don’t create futures worth supporting.

I’m with you, any of them could succeed but BTC is just a cosmetic upgrade of the status quo and BSV far too easily lends itself to an Orwellian dystopia.

A case can be for the success of other coins, but the cryptocurrency that dominates the market in the future will be the one which is used as a medium of exchange.

In How to Value Cryptocurrency: The Equation of Exchange, we walked through the steps to valuing a currency based on its utility. Eat Sleep Crypto tries to be as straightforward as possible, but valuing cryptocurrency based on utility is a paradigm shift from the still-speculative market.

I may have overestimated the article’s clarity, but I passed it to my grandma, who’s very sharp and capable of understanding the subject. This was her actual response:

Nate

I sort of understand your article. But why is another valuation method needed? Isn’t the value what someone will pay? I.e. what the coin will purchase?

Love,

Grandma

Disclaimer: My grandma is more well-versed in politics, economics, and business than most people I’ve ever met. I hope my response is concise enough for all grandmas, but your mileage may vary.

Cryptocurrency Price Factors

Grandma,

You’re thinking of it correctly. The ‘valuation’ is a loose price floor created by demand for goods in that currency.

For example, say Ford wants to buy $1000 worth of parts from China. Chinese manufacturers demand payment in a new currency, the Gold Yuan.

If there is only $500 worth of Gold Yuan in circulation, Ford can’t pay. However, by buying Gold Yuan – assuming there is some outside demand for the currency, Ford raises the price of Gold Yuan until their holdings are valuable enough to pay the manufacturers.

The principle here is that the money supply of an economy must be valuable enough to support purchases in that economy. In the absence of market-makers, volatility may push the price under this price floor temporarily.

Speculators can push the price infinitely high, but as long as commercial transactions exist, there is a loose price floor waiting at the bottom.

Market Demand For Cryptocurrency

I sent the first email. I tend to realize what I left out after sending an email – a terrible habit, not unlike leaving the house without your keys – my other favorite. So I quickly sent the following:

As it relates to cryptocurrencies – online merchants demand them.

Some demand cryptocurrencies on principle, more demand them for privacy, and half the world demands crypto because they don’t have access to traditional finance.

I write about cryptocurrencies which are adopted for the latter two reasons. Eventually they will become the standard.

Thank you for sending the previously linked article, and thanks for asking these questions.

Conclusion

This is a lightly edited version of an actual exchange between my grandma and I. She’s sharp, but anyone understand cryptocurrency when it’s explained in common terms.

Fostering understanding is Eat Sleep Crypto’s mission. We detest the deviations from utility-based investing principles. Speculation delays adoption and doesn’t work. The sooner the market gets on board, the quicker cryptocurrencies will be adopted by the world – particularly by those with no alternatives.

We write about valuing cryptocurrencies using each cryptocurrency’s utility a medium of exchange to mirror Warren Buffett and Benjamin Graham’s style of value investing, and have created several articles on individual cryptocurrencies with this lens.

Cryptocurrency investment has been almost entirely speculative. In 2017, anyone with a half-baked idea could write a whitepaper, create a token contract, and raise $50 million in a week-long ICO.

Besides Joe and Jane Sixpack, participants with larger allocations were BTC early adopters and Silicon Valley veterans who should have known better. Then again, everyone is a genius in a bull market.

It wasn’t until the bear market struck that these investors started second guessing their positions. Fundamentally, investors failed to understand that cryptocurrencies (and tokens) should be valued not as stocks or commodities but as currencies.

The Bitcoin model yields a $50 million dollar per BTC value in 2030 with default assumptions.

Fortunately, it’s not only possible to value cryptocurrencies on a fundamental basis, this type of appraisal delivers more accurate valuations than speculative targets, and fortune awaits those who identify these investment opportunities.

The Equation of Exchange

The equation of exchange is used by economists to model currencies. It has four variables which describe the relationship between purchases made in an economy and the amount of circulating currency. We can use this equation to assign a value to a currency based on its utilty…that is, its fundamental usage as a medium of exchange. This, after all, is what the genesis of cryptocurrency was all about.

The equation is

MV = PQ

M represents the units currency actually circulating in an economy. Hodl’d units don’t count.

V is for velocity. Velocity is the number of transactions an average currency unit will encounter, per year.

P stands for purchases. Its value is the average price of purchases in an economy.

Q is the quantity of these average transactions.

Given any 3 of these variables we can determine the 4th. Now for some application.

In the US, M1 is the term for all dollars circulating in the economy. According to the St. Louis Fed, dollars are used an average of 5.5 to 6 times per year so we’ll use a V of 6.

Suppose that the average purchase in the US is $50 (P=50), and that the yearly quantity of these purchases is 20 (Q=20).

Therefore, PQ is $1000 and through the equation of exchange must be equivalent to MV. (MV = PQ)

So, what we know is:

P = $50

Q = 20

PQ = $1000

MV = $1000

V = 6

Given a velocity of 6, we can solve for the remaining variable M, the monetary base. To do this, we divide both sides by 6.

This leaves us with M = $1000/6 = $166.67.

And voilà, with only three variables, we’ve just calculated the total monetary base of an economy.

This can be solved for any size economy, but the relevance to cryptocurrency is that the equation of exchange can be applied to specific use cases targeted by niche cryptocurrencies. Let’s look at one now.

Example B: WidgetCoin (WGC)

Imagine WidgetCorp sells widgets for an average of $20. Five hundred of them are purchased per year for an annual volume of $10,000.

Q = 500, P = $20

Now suppose as the sole manufacturer of widgets, WidgetCorp decides to create WidgetCoin (WGC) and require payments be made in WGC. WidgetCorp also has a monopoly, (state-sanctioned of course).

Because it’s a closed system, the new currency has its own velocity. Some speculators are reluctant to spend their WidgetCoins, so we’ll estimate a WGC velocity of 4.

Now we can solve for the monetary base required to support purchases, M, i.e. the value of circulating WidgetCoins.

M * 4 = $20 * 500

4M = $10,000

M = $2,500

So we’ve figured out that the total value of circulating WGC is $2,500, but what is one WidgetCoin worth?

We could simply look at the market price, but price won’t tell us what the actual value is. WGC could be fairly valued, overvalued or undervalued, and as investors this is what we want to determine.

We seek the intrinsic value of a WidgetCoin. To calculate that, we need a critical piece of information – the circulating supply of WGC.

There may be a thousand, ten thousand, or millions of WGC but let’s imagine WidgetCorp was conservative in determining token supply. WidgetCorp wanted each widget to cost 100 WGC, and they issued 12,500 coins.

With the known dollar-value of the monetary base, we can factor in the coin supply to calculate the expected market value of each coin.

In this case, $2,500 divided by 12,500 coins is $0.20 per coin.

Now pretend WidgetCorp instead decided to create 1 million coins.

The same $2,500 divided by 1,000,000 coins is $0.0025 per coin – a quarter of a penny.

If WidgetCorp had ICO’d WGC for 20 cents each, they’d have made a killing. Unfortunately, early investors would have seen the value of their WGC fall by 98.75% as the market adjusted.

Wittingly or not, this is what happened in 2017 with ICOs.

It’s also the reason behind Bitcoin volatility. The market price strays from Bitcoin’s intrinsic (i.e. utility) value.

With largely speculative transactions, Bitcoin’s economy has no fundamental drivers of value – no necessary purchases (PQ). Eventually, the market catches on and adjusts the price accordingly.

For a more in-depth exploration of Bitcoin’s intrinsic value, go to Investor Series #1. (At this point, you’re well-equipped enough to skip the first part and go straight to the calculations.)

Implications

The equation of exchange is not only relevant to ICOs, or Bitcoin. The equation of exchange is the single most important equation in the industry, and yet it’s been largely ignored. Eat Sleep Crypto applies it, and you should too.

As the bear market eats weaker currencies, we focus on the value propositions of utilitarian coins in niche markets. Hope is not an investment strategy.

These currencies are the subject of our Investor Series. Our next edition is due this week and will be offered at a discount exclusively to subscribers of Eat Sleep Crypto. We’re covering Monero, one of our favorite coins, and the determined value will shock you.

Keeping with the “utility determines value” theme, free analysis is readily available on Reddit and Facebook, and is worth exactly what it costs. However, if you want to know what we know, it’s going to cost you something.

Right now though, you can get a preview for free.

Sign up for a 5-day free trial of the Eat Sleep Crypto daily newsletter and send us a message to receive a notification when we release Investor Series #3 – Monero.