If you’ve spent any time on this site, you’re likely familiar with the Equation of Exchange, MV = PQ.

This simple equation, first derived by John Stuart Mill and later popularized by Milton Friedman is the foundation of all our work.

The equation of exchange can be applied at a high level to quickly calculate price floors of a currency based on a few inputs or assumptions.

It can also be applied at a micro-level to tweak the economics and incentives of a cryptocurrency or token for maximum value capture.

If any of these terms are unfamiliar, you can refer to the Glossary page for their definitions.

Goals of this project

Token analysis script

Token flow visualization

Token engineering framework

Token economic analysis

The first goal of this project is to create a script that parses transaction data of a given cryptocurrency or token in order to find components of its price floor according to the equation of exchange, MV = PQ.

Simple pulls include contract events and token transactions that take place within the token protocol to find PQ. Calculated components include circulating supply and address balances over time to find V.

Token flow model

Using variants of the equation of exchange, token flow can be modeled within an ecosystem.

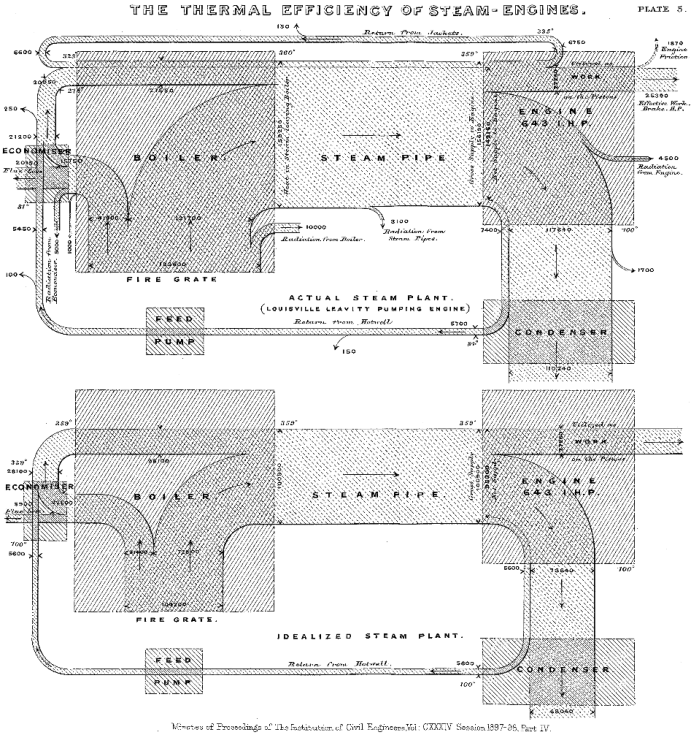

A novel way to do this is by using a Sankey diagram.

The Sankey diagram takes its name from Irish Captain Matthew Sankey, who used it to model the energy efficiency of a steam engine.

Sankey compared the real energy efficiency of an engine to its ideal efficiency.

While Sankey was interested in energy efficiency, we are interested in value capture.

Value is most commonly captured by tokens when they are used as a medium of exchange, denominated in another separate unit of account – e.g. an expenditure of $10,000 worth of Bitcoin.

Components in a token flow diagram

Objects in a token flow diagram represent participants in the ecosystem within which a token circulates.

Value transferred via transactions is represented by the connections in between.

The dimensions (height x width x length = volume) of the “pipes” representing these connections represent:

Tokens circulating in an ecosystem (circulating supply)

The value transferred between participants in an ecosystem (PQ)

The time a token takes to circulate, represented by length of all pipes (V)

Token flow diagrams denominated in native units (e.g. BTC) and those denominated in another unit of account (dollars) can be overlayed to solve for the price floor of each unit.

In this way, token flow diagrams become a visual aid in calculating price floors.

Token economic engineering

Sankey diagrams are fitting for token flow visualization for more than one reason.

Sankey’s hallmark example of a steam engine makes for an excellent analogy to token ecosystems for our purposes of designing and refining the token economics of a protocol, token economic engineering.

Like steam engines, cryptocurrency protocols have mechanisms which direct the flow and efficiency of energy.

In our models, energy is economic “potential” energy, represented by tokens with purchasing power.

Keeping with the steam engine analogy, the “goal” of token economic engineering is to first to increase the volume of the pipes, and second to decrease the number of tokens flowing through them.

We discuss various ways to do this on Telegram, and we collaborate with each other in reaching the goals described above.

If you’d like to collaborate, send a message to @EatSleepCrypto on Twitter for an invite.

Under this scenario, agorists, voluntaryists, and crypto-anarchists imagine a technocratic dystopia, in which none are free from the watchful eyes of the government-tech coalition.

Due to their independent-mindedness, dissidents would find themselves excluded from the mainstream financial system, severely limited in their travel, with only a barter economy and perhaps precious metals as a medium of exchange.

It’s a nightmare of a vision, but thankfully, things don’t seem poised to develop that way – at least not to the extent many imagine.

That’s because even a cashless society, cryptocurrencies will still be accessible and liquid.

Even if cryptocurrencies are fully banned, there will be loopholes.

General government incompetence, and the limited will of the state to enforce its laws guarantee necessary space for agorists to operate.

It isn’t entirely likely in a cashless society that cryptocurrencies would receive a full ban. Politicians always leave themselves an out, and cryptocurrencies are second only to cash for preserving financial privacy.

Cash is extremely useful to politicians accepting bribes and laundering their ill-gotten gains. They are simply unlikely to let such a tool go without a suitable replacement.

Bitcoin Cash in a cashless society

Bitcoin – a placeholder for decentralized, scaleable cryptocurrencies – is more than we know.

It will be the rails of the counter-economic underground railroad. This term, borrowed from Derrick Broze describes the infrastructure agorists, voluntaryists and the like will need to transact freely in a cashless society.

The vast majority of these innovations are happening on Bitcoin Cash, which at present is also the only cryptocurrency with such capabilities that has proven its security model and can actually scale to meet demand.

Today marks Bitcoin Cash’s third anniversary of independence from BTC. So we celebrate all of Bitcoin Cash’s innovations and look forward to its future contributions to the counter-economic underground railroad, and the freedom it enables.

As the first industry to operate in a truly free market, cryptocurrency is by nature the most competitive industry in the world.

There are many competing implementations of the idea of cryptocurrencies, and even more ideas on how cryptocurrencies should and even do operate.

How does one discern truth among all the competing claims?

Everyone on Earth has frameworks, worldviews, lenses through which they see and interpret events.

In crypto, we call these narratives.

Narratives are helpful in contextualizing and integrating information, but when relied upon too heavily, they obscure truth and exclude data from consideration.

Predictive capability

No narrative is perfectly correct; all lack some nuance. Yet narratives are necessary for human comprehension. The key is finding the right one.

But how does one know the narrative they subscribe to is correct?

In statistics, models are judged as useful or “true” according to their predictive ability.

Narratives in line with reality facilitate the correct prediction of future events.

Weekly Newsletter topics

This week, a number of things happened which destroyed the dominant narratives.

These events were explicitly predicted by several of cryptocurrency’s best and brightest.

The narrative here was encapsulated in the meme “Institutional [money] is coming.” Bitcoin speculators have based much of their optimism in the perpetuation of the BTC pyramid scheme on the eventual buy-in of institutions.

The Bakkt network – a creation of the Intercontinental Exchange, owner of the NYSE – disappointed investors so hard that JP Morgan said it caused a 25% drop in the price of Bitcoin (BTC).

Sept. 28th – Lightning bug

Another of BTC speculators’ theories is that the Lightning Network – an perpetually unfinished work – will soon scale and solve all of Bitcoin’s usability issues which were brought on by developers’ refusal to increase the block size limit.

A critical bug was “discovered” in the Lightning Network which allowed users to spend bitcoins that didn’t exist. Calling this bug critical is an understatement.

There’s nothing wrong with expecting technological advances to solve problems (see Moore’s Law). The issue with the Lightning Network is that a) evidence has been to the contrary since its inception, and b) basically all of BTC’s hopes of scaling in a decentralized manner were gambled on Lightning, which has perpetually fallen short of expectations.

In anticipation of this, a few developers created Bitcoin Cash, which is the continuation of Bitcoin as it used to be – fast, reliable, and cheap to use. The Bitcoin Cash community – mostly made up of long-time Bitcoin supporters – has also been predicting very underwhelming institutional interest in BTC.

Oct. 1 – UK Crypto regulations

As the Bakkt flop showed, “institutional” is probably not coming. Neither is it desirable. With institutions come regulations. This week, CoinShares sent out a request for comments on the UK Financial Conduct Authority’s intent to ban retail access to cryptocurrency derivatives.

In short, a healthy derivatives market allows more participants by making it less risky for smaller players. The only reason to ban these is that derivatives would make cryptocurrencies more stable.

Retail access to cryptocurrency derivatives is already extremely limited; as the non-events of Bakkt show, the institutional interest barely even exists. Governments are seeking to prevent the creation of such an ecosystem. If cryptocurrencies become stable, government-mandated fiat currencies lose their appeal, and then governments lose their hold on people.

This move will confuse those whose narrative suggests that governments will support the growth of the cryptocurrency ecosystem. With few exceptions, the broad swath of politicians and agencies are vehemently opposed to cryptocurrency adoption.

The narrative that’s predicted this holds that governments and other major players in the “money industry” want to shut cryptocurrencies down.

This view is held by a minorityin crypto.

Due to their preconceptions, the majority of the cryptocurrency community believes that BTC is the frontrunner for bringing financial freedom, or long-term success to the crypto space.

Bitcoin’s opponents attempt to stop it by twisting the narrative of its supporters.

First, they introduce a perversion of an accepted narrative (e.g. Bitcoin as digital gold rather than electronic cash). Then, they change the protocol once the narrative gains critical momentum.

Luckily, narratives which are out of touch with reality doom those who operate by them to failure.

The expected value of a flawed model is false conclusions.

A subset of people in cryptocurrrency have a staggering history of correct predictions, and it’s these people we subscribe to. Through earnest reflection and examination of ideas, we hope to create more of them.

Bitcoin dominance denotes the percentage market share Bitcoin has among all cryptocurrencies.

The metric made sense at its inception, though there was little need for other cryptocurrencies in 2013. It was assumed that Bitcoin would scale to handle all possible transactions.

Now, Bitcoin dominance is used to compare Bitcoin (BTC) to every other cryptocurrency – without regard to the fact that BTC is no longer a currency, nor does it aim to be one.

After Bitcoin was co-opted by globalists and the Bitcoin community split into two, the BTC branch started promoting Bitcoin as ‘digital gold,’ while the other side of the community became Bitcoin Cash (BCH) and promotes Bitcoin as cash.

Apples-to-oranges comparisons

Because BTC is no longer a currency, it seems ill-fitting to compare it with actual cryptocurrencies like Bitcoin Cash, Dash, and Monero.

Apples-to-apples comparisons would use TAMs to compare cryptoassets with the same niches.

Actual BTC dominance

By this standard, BTC’s dominance is nearly 100%; no other cryptocurrency is as slow and expensive to use as BTC.

Through a host of cognitive biases, BTC maximalists have actually convinced themselves these are desirable properties for Bitcoin, since they are also features of gold.

We’re speaking somewhat tongue-in-cheek, but BTC is actually the only cryptoasset pursuing “store of value” uses for a Total Addressable Market.

Other TAMs

As we mentioned above, cryptocurrencies have a separate niche from ‘digital gold’. Cryptocurrencies like Bitcoin Cash, Dash, and Monero address the ‘medium of exchange’ market.

There are also many niches for blockchain applications to disintermediate. Many ICOs issued tokens designated specifically for this second niche.

Platform tokens

Through the 2017 ICO wave, speculators learned that separate currencies are unnecessary for specific niches. Most use cases of a blockchain can use the blockchain’s native asset, or a stablecoin built on it.

The blockchains underlying applications are generally called platforms; we call their native assets platform tokens.

Ethereum and ETH are one such example.

Platforms fit a large niche with several sub-niches, each with a corresponding TAM. In making comparisons, it would make sense to compare the supply of these platform tokens to each other, rather than to BTC, or to cryptocurrencies like BCH.

Conclusion

BTC used to be fast, cheap, and reliable – it used to work like Bitcoin Cash.

Now when BTC fees increase, people use other cryptocurrencies. The only context in which it makes sense to compare BTC to Bitcoin Cash (BCH) or Ethereum (ETH) is in the amount of money flowing into the ecosystem through each asset.

A new metric or series of metrics is required to measure dominance between cryptoassets.

For now, we’re specifying the TAM of each currency in our Investor Series articles and models. If there’s demand for it, we’ll create charts to classify cryptocurrencies according to target markets.

Let us know in the comments what you’d like to see in future articles, or in follow up to this one.

The question is compelling because it’s real. It’s easy to balance two, but a blockchain with all three is still theoretical.

Bitcoin Forks

Bitcoin has been forked innumerable times, but the Bitcoin community has only forked twice – creating three separate chains.

Each of these chains correspond to a position in the “blockchain trilemma.”

BTC

The fork of Bitcoin known as BTC chose security and decentralization.

By limiting the amount of transactions which could fit in a block, BTC ensures that miners will never get so large that they can be coerced by malicious actors.

BCH

Bitcoin Cash (BCH) forked over BTC’s decision to keep the blocks small, and transactions limited, because small blocks cause high fees, and high fees limit the potential user base – rendering Bitcoin (BTC) useless as cash.

The (short-term) sacrifice BCH made was security, and to some extent decentralization, but the community’s support of the coin is exercised through the market; if decentralization were to falter, the market would punish holders of BCH and therefore miners and developers.

Regarding the trilemma, BCH chooses decentralization and scalability.

BSV

That leaves one position for the third and final fork. Bitcoin Satoshi [sic] Vision (BSV) chooses scalability and security.

Conveniently, BSV supporters deny that the trilemma even exists. Nevertheless, it’s quite clear to everyone outside their cult why they’ve chosen this. It has to do with the political ideologies of those involved.

Solutions to the Trilemma

Between those forks which acknowledge the blockchain trilemma, third-party solutions to it have been suggested.

BTC’s solution is the Lightning Network, supposedly trustless and decentralized, but not so in practice. Without a trusted oracle to keep nodes aware of the state of the network, formation of centralized hubs is inevitable.

Pending its success in a testnet environment, Avalanche is one solution for Bitcoin Cash. Avalanche is similar to the theoretical Lightning Network in that it would shore up BCH’s weaknesses dictated by the trilemma.

We’ve linked the latest example, which just so happened to be yesterday – we Googled the recurrent problem and that came up.

Conclusion

This problem is not unique to Bitcoin forks. Every blockchain is trying to solve the blockchain trilemma – even BSV; the problem still exists.

This framework is helpful for contextualizing Bitcoin forks thus far, and may be helpful in predicting future Bitcoin forks.

While there are only three possible answers, according to the structure of the question posed by Gabriel Cardona, in practice, blockchains may include some level of each.

The extreme positions resulting from “pick two” are merely illustrative.

It’s possible that in the future, should the market call for further forks, that splits will be along these lines – for example, an emphasis on scalability over decentralization, or in varying degrees of all three.

Bitcoin forks have caused a financial bloodbath and vicious animosity between community factions, so we hope there are no further forks, but (thankfully) that’s not up to us – the market determines whether a fork is prudent or not.

Decentralized finance is the next wave of applications on scaleable cryptocurrencies, for which Bitcoin Cash is preparing.

Examples of existing DeFi components include stablecoins, and tokenized assets.

One perspective is that DeFi distracts from the main purpose of cryptocurrencies as a medium of exchange.

Bitcoin entrepreneur Vin Armani has been proposing a different idea – “Bitcoin [broadly defined] is not money.”

Because of Bitcoin’s ability to make assets like property titles and even fiat currencies digitally native – tokenization – Vin proposes that Bitcoin is essentially a value transfer network.

While some tokenized assets present security risks for Bitcoin Cash through economic abstraction, use of certain types of tokenized assets will magnify the increase in BCH’s price as they are created – thus incentivizing greater security by increasing the network hash rate.

“Backed” stablecoins

Tether was the first generation of stablecoins – cryptocurrencies which stay at or near a $1.00 value, despite major volatility in the prices of the networks on which they’re hosted.

As the first of its kind, Tether was justified in its rudimentary attempt to do this using a trusted third party.

However, Bitcoin was created to eliminate the need for trusted third parties – instead using math, game theory, and economic incentives to guarantee secure value transfer.

The next generations of stablecoins must incorporate these principles to become similarly trustless.

Algorithmic (collateralized) stablecoins

Dai is a recent stablecoin, built on the Ethereum blockchain. For the visually inclined, here’s a one-minute video explanation.

Dai maintains a 1:1 peg with the USD through a decentralized autonomous organization (or DAO).

While Dai is a novel concept, it bears many parallels with the US Federal Reserve. MakerDAO issues DAI in exchange for the ETH – Ethereum’s native asset – from borrowers.

Like the Federal Reserve Board, MakerDAO lenders vote to set interest rates, which in turn affects the price of the DAI token.

Interest rates can be raised to dissuade potential borrowers, which would decrease the value of the DAI token, or vice versa to increase it.

When borrowers return DAI, they receive their ETH back, minus the interest – called a stability fee.

This works because DAI is overcollateralized by ETH. Should the price of ETH fall sharply in a short time frame, in theory, the MakerDAO could vote to decrease interest rates.

Liquidation of collateral is also possible, but hasn’t been necessary to maintain Dai’s 1-to-1 USD peg.

Traditional backed assets present a security threat to the base layer

In Tether’s case, a theoretically infinite amount could be issued on any chain, without a corresponding change in the price of that chain’s base asset.

For example, one trillion Tether (USDT) issued on the Ethereum chain would not directly affect the price of ETH.

The transfer of tokenized assets is only as secure as the blockchain on which they’re issued.

Security, in turn, comes from the fees paid to miners to maintain the network by honestly recording transactions.

Without enough security, miners could defraud the network, making a payment, then reversing it after receiving the other side of the presumed exchange of goods or services – a double spend.

For this reason, backed stablecoins present a double-spending hazard if the value they transfer exceeds the cost of a double-spend.

The security of a network which prevents this – measured by the hash rate of that network on a proof-of-work chain like Bitcoin or Ethereum – follows the price of the chain’s native asset.

Value capture dynamics of stablecoins

Stablecoins like Tether, which don’t necessarily increase the price of the underlying blockchain’s native asset are subject to double-spending as the value they transfer increases, but the value of the native asset remains unchanged.

By contrast, Dai and other algorithmic stablecoins increase the price of the underlying asset through collateralization.

Dai does this in two ways:

First, the price increases when the collateral asset, ETH is purchased. Then, subsequent lockup of funds decreases circulating supply of coins, increasing the value of those outstanding.

This phenomenon is magnified in Dai’s case because positions are overcollateralized – there is a greater lockup of ETH than the value is issued in Dai.

Again, the higher price of a blockchain’s base asset attracts miners, which provide security; hash follows price.

In this way, collateralized stablecoins offset risk of double-spending otherwise encouraged by backed assets.

This hazardous phenomenon is known as economic abstraction.

Conclusion

Stablecoins will be required to build more useful, user-friendly financial applications on Bitcoin Cash.

Algorithmic stablecoins are preferable to backed stablecoins because they offset the risk of double spends by increasing the price of the base asset – a benefit in itself.

All this while maintaining censorship resistance, since assets remain on chain; with algorithmic stablecoins, trusted third parties are not required to exchange assets.

This is a major step toward more powerful financial applications on Bitcoin Cash – the only real frontrunner with an on-chain scaling plan that is open to these.

“Bitcoin is digital gold” is a popular trope among Bitcoin (BTC) maximalists due to its scarcity and [former] use in payments.

Bitcoin had obvious advantages over gold, Bitcoin Core developers destroyed these after ousting Satoshi Nakamoto’s handpicked successor and those who supported his vision.

Bitcoin’s unique value proposition was as a permissionless payment network with a native asset.

Digital dollars require a Visa, Paypal, or SWIFT to move through; cryptocurrencies are native to their networks.

Bitcoin scaling and high fees

Contrary to Satoshi Nakamoto’s advice, Bitcoin Core developers artificially limited the amount of transactions Bitcoin could process.

This created a bidding war for block space, driving fees up to ten, fifty, even hundreds of dollars per transaction in some cases.

Apologists like Safidean Ammous argue that this is how Bitcoin is supposed to work; some developers are even campaigning for less space for transactions each block.

A new analogy

Maximalists’ reasoning that difficult, costly transactions are desirable because they mimic gold is clearly absurd – a dogmatic fixation with reasoning by analogy instead of from first principles.

Yet, the analogy conveys a potent message: Like gold, Bitcoin is scarce and durable, and therefore valuable.

Analogies can be useful in teaching, but all analogies break down in some detail. “Digital gold” misses Bitcoin’s unique nature as a payment network AND its native asset.

If we are to continue introducing newcomers to cryptocurrency by analogies, a new analogy is in order – and one that highlights cryptocurrencies’ unique utility.

“Digital Platinum”

Gold is not an especially useful metal.

Most of its “use” is as a speculative instrument, or else as a display of wealth – a feature not replicable by Bitcoin.

Among precious metals, copper is arguably the most useful, but it’s not scarce. Platinum lies somewhere in between.

Digital platinum makes for a better analogy, especially for Bitcoin Cash, which follows Satoshi’s outline for scaling that affords it utility.

True to the analogy, platinum is even used in its own mining, found in the catalytic converters of the heavy machines which harvest the ore.

Conclusion

No analogy is perfect; taken to extremes, this one would fall apart as well.

For the purpose of informing the next wave of cryptocurrency users, though, “digital platinum” should do.

Hopefully we won’t need to write another article in five years clarifying the intent of this one.

“Blockchain, not Bitcoin” is a common refrain from those skeptical of cryptocurrencies.

Is the technology underlying Bitcoin better suited for other purposes, and if so, what are they?

Furthermore, if these are valuable solutions, why haven’t they been developed yet?

We’ll answer these questions in the following few paragraphs.

What is a blockchain?

Blockchains are basically redundant databases.

Think one-hundred-entry accounting.

All of those entries are public, so anyone can verify them.

Most companies don’t want completely transparent books, and most public data isn’t worth paying 100 times (or more) the standard rate to store.

Most data doesn’t need the redundancy/transparency that blockchains offer, but some does.

Data which is at risk of being censored or tampered with may be worth paying one hundred times the price to store on-chain.

Decentralized applications (dApps)

Applications built on decentralized blockchains are called dApps.

Most of the dApps which have been created have too much data to fit on a blockchain, or don’t require censorship resistance to begin with.

There are a few good decentralized applications, though.

Even these would be better on traditional database, but due to high risk of censorship (from governments), they are impossible for centralized companies.

Voting

Transparent vote tallying is one application of a blockchain.

It’s cheap to send a transaction on most blockchains, and small bits of information (e.g. a candidate’s name) can be included for less than a cent.

Votes could be tallied manually with references to immutable data.

Because of scale, this is much more practical on a local level, but could be done on a state or national level on a blockchain with high transaction throughput.

Prediction markets

Prediction markets are another application for which blockchains are well-suited.

Prediction markets allow users to create customized bets on future events, then trade those positions with others.

The price of a position in a prediction market reflects the market’s assessment of the event’s probability.

This would enable risk-averse companies to hedge their bets on future events, signal an issue’s importance (looking at volume), and could even guide public policy.

Censor-proof social media (hybrid)

Most of social media is clutter. Selfies and cat videos and don’t need censorship resistance.

But as Facebook, Google, and Twitter have shown, certain political positions are unwelcome in public discourse.

Users, most often libertarians and conservatives have been banned from these platforms on the grounds of “hate speech” for promoting rational positions.

Conservative social media sites like Gab have popped up to make a home for some of these, but even Gab has been censored, cut off from payment processors.

Furthermore, Gab is a company, and could easily censor a liberal faction of its user base, for example.

To prevent this, social media companies could employ a hybrid database architecture – optional archival of posts on-chain.

This could be very useful for posts which are controversial or political in nature.

Archiving data

Cryptocurrency transactions are just strings of letters and numbers, so any kind of data can be posted to a blockchain.

If it’s worth it to the user who posts them, pictures, videos, and even large files can be hosted on a blockchain.

It’s been three years since high-profile dApps which fueled the ICO craze of 2017 debuted.

Of those, only one which requires a blockchain actually came to fruition – Augur, a prediction market app built on Ethereum. Other attempts at prediction markets are imminent on the Bitcoin Cash chain.

Prediction markets are extremely underestimated by the public and could drastically impact future events.

For more reading, check out the Wikipedia page on the subject.

Conclusion

Blockchain is still a somewhat nascent technology. It would be foolish to rule out future applications entirely, but so far, these are the only decentralized applications beyond money and other property which make sense.

And there’s a common thread with all of these. Some of them are subversive, but all of them require decentralization due to threat of government force.

Absent this coercion, even prediction markets and social media would be safe from censorship – competition would force bad actors out of business.

By enabling the first truly free markets, cryptocurrencies allow these beneficial technologies to help humanity reach its next steps toward freedom.

Bitcoin has been on some wild rides the past few years. Hitting a crescendo of $20,000 in December 2017, BTC dropped to $12,000 just days later and stumbled down to $6,200 over the next two months.

Many people panicked: some trading in and out, others HODLing all the way down. Weathering 80% losses takes discipline, but the promise that Bitcoin might boom again keeps speculators invested. Bitcoin’s history of consistent, outrageous returns is compelling for those taking a long view. “Taking a long view” requires understanding three principles: objective valuation, technical developments, and factors surrounding adoption.

For traditional investors, this speculation looks foolish. “Where are the fundamentals?” they ask. Volatile returns engender speculation, and speculation spawns volatility. High volatility plus a lack of a traditional valuation mechanism generally screams ‘pyramid scheme’ and forces more conservative investors to abandon the field to speculators. And round and round we go.

Cryptocurrency Valuation

Bitcoin, like all currencies, derives its value through use as a medium of exchange, and I’ve already demonstrated that it can be valued according to the accepted equation of exchange: MV = PQ. This equation shows that the price of a currency must be high enough to support the purchases made with it.

To illustrate this principle, let’s imagine Alice wants to buy a car from her friend Bob. (yes, for the love of Mike, it’s Alice and Bob again). Both Bob and Alice agree that the car is worth $1,000, but Bob demands to be paid in his own currency: Bob’s Car Coins (BCC).

The question immediately arises, how much is each BCC worth?

For an established currency, we could look to market data, but there is none. BCC is an entirely new currency.

Let’s say Bob wants 10 BCC for his car, but Alice has no BCC. Assuming she can exchange dollars for BCC, Alice is willing to pay up to $100 per BCC in order to purchase the car (10 BCC multiplied by $100 per BCC equals $1,000.)

In this transaction, Bob doesn’t explicitly tell Alice the price of each BCC, but he does give his currency value by choosing to accept payments in it. In this example, we see the axiom that the value of a currency increases to support the purchases being made with it.

Speculation can move prices temporarily, but use as payment establishes a currency’s worth.

There are two aspects to the determination of value through fundamental analysis: applying economic principles, and data extrapolation. In cryptocurrency valuation, the second informs the first.

Economic Principles

As illustrated in the example, using a currency as a medium of exchange gives it value. We see this principle applied in the equation of exchange. Fundamentally, if we know the total value of purchases with a cryptocurrency and the velocity of the currency, we can determine the price of each unit. Velocity is the average number of times a unit is ‘recycled’ in a specified time frame. With these variables, the equation of exchange (MV = PQ) is easy to solve algebraically.

Rewritten to solve for M, the monetary base, the equation of exchange reads M = PQ/V. You can read the full explanation in previous Eat Sleep Crypto articles. In short, this means that the value of circulating currency is equal to the total value of purchases made with that currency, divided by the average number of times a unit of currency changes hands.

After solving for M, we can determine the value of each unit by dividing M by the circulating supply of each coin. We do this in several examples on Eat Sleep Crypto, including the Investor Series #1 – Bitcoin valuation article.

Data Extrapolation

While it appears satisfying and conclusive, fundamental analysis is not the only approach to currency valuation. We can also forecast future prices based on expected use of cryptocurrencies as a medium of exchange. In the Bitcoin article, we use the SWIFT network as a proxy for global transactions. Data extrapolation, in this case, involves substituting Bitcoin for the SWIFT network. Our model yields a conservative estimate of $50 million per bitcoin by 2030, employing our own assumptions. (If you’re interested in seeing a copy of our model, say something in the comments below.)

$50 million per bitcoin may sound like hyperbole. It’s not. The SWIFT network does over a quadrillion dollars in transactions per year: a thousand trillions!

This analysis doesn’t factor in transactions from commercial payment systems like Visa and Mastercard, Paypal, or cash payments, all of which are vulnerable to replacement by crypto. But, it does assume adoption of crypto as a medium of exchange, when in reality immediate adoption is not the top priority for most cryptocurrency developers.

Despite the justifications referenced above, some proponents of Bitcoin continue to dismiss it as a medium of exchange. There are two reasons why. The first is the “store of value” narrative and the second is Bitcoin’s “greater fool” theory.

Bitcoin: A Peer-To-Peer Electronic Store Of Value

People who promote Bitcoin as a “store of value” argue against its use as a medium of exchange. Discounting entirely that Bitcoin is far too volatile to be a store of value in the short term, there is so much irony in this position. As good “stores of value” need fundamental properties to make them desirable, good currencies are inherently stores of value and command higher prices because of it.

The long term value proposition of Bitcoin or any other cryptocurrency is significantly greater as a medium of exchange than as a store of value. Estimates of Bitcoin’s value if it replaced gold entirely is only $4 million dollars per coin. That’s more than an order of magnitude less than its conservative value as a medium of exchange.

While the BTC community fritters away it’s first-mover advantage, most other cryptofolk are driving adoption where it’s needed least. If you think of cryptocurrencies as products solving a problem, you can’t help but see that the largest markets, in terms of numbers of customers, are being ignored

A large percentage of early Bitcoiners have first-world origins. Adoption evangelists have therefore been active in those countries – exactly where a volatile, traceable, alternative currency is of little use. While BTC supporters have rejected Bitcoin’s purpose as a peer-to-peer electronic cash system, even those who imagine scaling via the Lightning Network haven’t considered the technical and economic limitations of third-world users. Not to mention the limitations of the Lightning Network itself!

Bitcoin’s Greater Fool Theory

Some advocates of Bitcoin believe that others will purchase Bitcoin because of greed and fear of missing out. As a consequence, they drive the price up. These advocates assume BTC can scale and that it will eventually become a store of value once it reaches its final price. In their minds, this culminates with institutions FOMOing into BTC as an investment.

These arguments imply that cryptocurrencies have no fundamental drivers of value. In reality, cryptocurrencies have a stronger value proposition than almost any other asset class. Because of blockchain’s transparency, we’re able to quantify cryptocurrencies’ worth.

The Importance of Adoption

Many cryptocurrency advocates across communities imagine that cryptocurrency will take hold in places like the US and Europe, and then gradually catch on in third world countries.

The reality is, first world users don’t need Bitcoin. But Venezuelans do.

Ironically, if adopted as a medium of exchange or “means of payment”, cryptocurrencies would see less volatility and eventually be adopted by the first world for payments. This decrease in volatility happens within an economy as purchases of the currency happen more frequently. A larger volume of commercial transactions offsets currency volatility. Further stability comes as goods and services are denominated in it.

Price Denomination

The denomination of goods and services in a currency creates strong price support. A quick thought experiment suggests that if someone knows they can buy the same meal for 0.1 BCH each time, they’re able to benchmark the price of other things in it, too. The axiom here is that people value a currency based on what it buys.

This is the same principle we see in our illustration with Alice and Bob. We can value each BCC Alice received from Bob at $100, despite neither of them officially setting the price. In this case, it was because we know that each BCC got Alice 1/10th of a $1000 car.

Closing Thoughts

With widespread adoption as a medium of exchange, Bitcoin, or any cryptocurrency, will become more stable due to the volume of purchases.

The key here is that ‘stability’ is relative. It’s relative to the price of goods, and the price of other currencies. Compared to a currency like Venezuela’s bolivar with 1,000,000% inflation against the USD, Bitcoin’s 80% drop is nothing. Fittingly, it’s through adoption in countries like Venezuela that cryptocurrencies can gain the necessary stability for worldwide adoption, while filling desperate demand for a sound currency.

With all this in mind, I was thrilled to hear about Bitcoin.com’s recent announcement of the initiative to onboard 500 merchants a month in Venezuela. Adoption like this raises prices and reduces volatility. The more adoption a cryptocurrency has as a medium of exchange, the more valuable it will be, and unlike a purely speculative asset, its volatility actually decreases with volume.

I’m looking forward to seeing meaningful adoption of all cryptocurrencies, and eager to see the shift in focus of cryptocurrency users from speculation to fundamentals as we witness the benefits that cryptocurrencies bring to the world.

Yesterday, JP Morgan Chase & Co released a note on Bitcoin’s intrinsic value.

Their analysis suggests Bitcoin is overvalued at $8000, citing a deviation from the costs of production.

BTC is overvalued, but not because miners are making a profit.

This argument has been floating around the Bitcoin space for a while. The position JPM takes is that “price follows hash.”

It’s also called the Labor Theory of Value and has been popularized by fans of Karl Marx.

The Labor Theory of Value opposes common sense; products are not valuable because they take effort but because they have demand, which implies utility.

Why Price Appears To Follow Hash

Price and hash are strongly correlated, but few take the leap of suggesting an increase in hashrate causes price to increase.

In March, Eat Sleep Crypto newsletter subscribers learned the mechanism behind the seeming causation.

Many Bitcoiners recognize a relationship between price and mining power (hash). The debate has been reduced to “price follows hash” vs “hash follows price.”

As usual, the truth is nuanced.

In a bull market, hash follows price. Miners choose to mine the most profitable coin.

In a bear market, price follows hash as miners with different costs undercut each other.

BTC dropped from $6200 to $3200 during the BCH/BSV hash war in November. The drop from $6200 to $5600 saw 30% drop in hash rate from the network. At the time, 70% of Bitcoin miners were in China.

It was logical to conclude the 30% became unprofitable and switched off, leaving the rest to sell at whatever price buyers would negotiate. I’d read that the cost of mining in China was around $3200 and placed my bets accordingly.

BTC bounced at $3150.

This was a confirmation of my theory and spurred further thoughts on how to fundamentally value cryptocurrencies.

During this time, we also saw refutations of competing theories – namely that “price follows hash,” or Marx’s Labor Theory of Value. Both Bitcoin Cash (BCH) and Bitcoin (SV) saw a surge in hash power, yet both of their prices decreased over the hash war.

Excerpted from the ESC newsletter, 3/27/19

In a bull market, hash follows price. In a bear market, price only appears to follow hash.

This framework explains the seeming correlation of price and hashrate in a bear market. Hopefully, it puts Bitcoin-related discussion of the Labor Theory of Value to rest.

If you enjoyed this article, check out the rest of the articles in the cryptocurrency valuation category.